Automatically deducting student loan payments from borrowers’ paychecks—and even tying the repayment amount to income, similar to Social Security withholdings — were among the ideas that seemed to interest Senators Thursday at a hearing to explore ways to simplify the federal student aid system.

Sen. Lamar Alexander, chair of the Senate Health, Education, Labor and Pensions (HELP) Committee, queried speakers at the hearing whether it would be a good idea to create a pilot program to test the idea as his panel prepares to start drafting legislation to reauthorize the Higher Education Act. The speakers noted that several countries already use such an automatic withholding, with exceptions for low-income individuals.

Much of the hearing was focused on improving the student aid delivery process, from the application form itself to students understanding the terms of aid agreements and repayment options. But panelists and some lawmakers cautioned that consolidating and simplifying should not result in shrinking the amount of aid available to students.

Beyond classroom costs

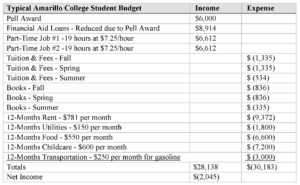

Russell Lowery-Hart, president of Amarillo College in Texas, said federal support needs to be about more than just paying for tuition and fees. In fact, for low-income students, it’s often the living expenses such as child care, housing and transportation that can prompt them to drop out. In Texas, community college students borrow $16,000, often on top of working, to finish their degrees, he said.

“The most powerful and debilitating barrier to success in the classroom for our students is poverty-related issues with transportation, child care, food, housing, health care, utilities and legal services,” he said.

It’s students with smaller student loan debt that tend to default more frequently, said Susan Dynarski, professor of Public Policy Education at the University of Michigan, noting that even “free” community college efforts typically cover just tuition and fees, and not living expenses.

Lowery-Hart highlighted efforts at his college to address those challenges, which included partnering with local social services programs such as food pantries, clothing closets and case-management systems, among others. This fall, the college’s social services system connected more than 1,400 students — which is 15 percent of the school’s student body — to services in one semester, he said.

Source: Testimony of Russell Lowery-Hart, president of Amarillo College

Offering such services has helped not only to keep students enrolled but also finishing their studies, Lowery-Hart said. At Amarillo College, intensive social services assistance has played a part in the college’s student success rate jumping from 19 percent over three years to 45 percent over three years, he said.

Lowery-Hart recommended that Congress increase federal funding for such programs. He also recommended increasing the maximum Pell award by $4,500, noting that the current maximum award covers less than half of today’s true costs to earn a college degree.

Start with the award letter

The hearing highlighted the fact that student aid recipients often get derailed right from the start — when they get a letter from their school outlining the financial aid they will receive. The award letters are not only confusing but sometimes misleading, said Laura Keane, chief policy officer at UAspire, which provides college affordability advising and advocacy to students and families.

“The award letters really trip up students,” she said.

Keane said a UAspire study found that about one-third of award letters list the direct cost of college, such as tuition and fees. Another one-third include both direct and indirect costs, such as books and transportation. And one-third don’t list any of the costs.

The study also found that the letters use varying student aid terms and definitions, and often lump together information about grants and loans, which further confuses students, Keane said.

Congress should also consolidate loan repayment options, several speakers noted. Currently, the federal government offers nine loan repayment options, and lenders often do a poor job of presenting the options to students, Dynarski said. They often select the one that means the least paperwork for them, rather than the one that best suits the student, she said.

Instilling annual loan counseling for students would also help, Keane added. Currently, students are counseled twice — when they receive the loan and when they “exit” it.

AACC efforts and next steps

As part of its HEA reauthorization agenda, The American Association of Community Colleges has advocated for many of the positions raised at the hearing. These include dramatically simplifying the income-based loan repayment, reducing the complexity of the student financial aid form, increasing Pell Grant funding and enhancing student loan servicing. Some of these ideas are including in legislation approved by the House Education and the Workforce Committee in December. The full House could act on that bill as soon as next month.

Alexander said he hopes his committee will send an HEA reauthorization bill to the full Senate by early spring. Sen. Patty Murray, the committee’s ranking Democrat, stated that she would like to have greater certainty about the U.S. Department of Education’s administrative actions as the process gets underway. The HELP Committee is scheduled to hold another HEA-related hearing on January 25, focusing on access and innovation.